Stablecoins are digital currencies that aim to be non-fluctuating assets similar to regular currencies used across countries to buy goods and services. The national currencies issued by governments are important in making economies function as, despite inflation, fluctuating exchange rates, and other factors, the value of most of these currencies do not fluctuate much in the short term. Stablecoins are pegged to a particular standard relative to which they attempt to stay stable, e.g. 1 unit of a coin pegged to USD would attempt to maintain the same value or price as 1 USD. There are different pegs that stablecoins follow such as commodities, fiat, or a combination of these. Since money cannot be created out of thin air, generally a stablecoin is backed by the value of an underlying asset or a system. Stablecoins are collateralized by fiat currencies such as USD, EUR, or GBP and held by a centralized custodian. Issuers of Fiat-backed coins claim that these coins are backed at a 1:1 ratio, meaning for each unit of coin there is one unit of real fiat currency (like dollar) being held in a bank account to back it up. These stablecoins are backed by some kind of commodity, such as precious metals like gold, oil, real estate. These commodities can even appreciate in the future, giving increased incentive for people to hold and use these coins. Digix Gold (DGX), is an ERC20 token that is backed by physical gold reserves, where 1 DGX is equivalent to 1 gram of gold. These are stablecoins backed by other cryptocurrencies such as Ether. As these stablecoins are backed by crypto which can be very volatile, they are over collateralized so that the collateral can cover for any sudden downward move in its price. This allows crypto-backed stablecoins to be much more decentralized than their fiat-backed counterparts since everything is conducted on the blockchain. To reduce price volatility risks, these stablecoins are often over-collateralized so they can absorb price fluctuations in the collateral. They are decentralized as the underlying assets are on-chain instead of being in a bank account. There is no single entity controlling users’ funds. Some platforms choose to use multiple cryptocurrencies as collateral in order to distribute risk. These are Stablecoins that do NOT have collateral to guarantee stability, but instead, they rely on different algorithmic systems to maintain the peg with fiat currencies. Since these coins are not collateralized by any asset, they are considered the most decentralized stablecoins. However, continual growth is needed for an algorithmic coin to be successful because in the event of a crash, there is no collateral to liquidate the coin back into, and users’ money would be lost. This means that there needs to be a consistent user demand for these coins as once demand falls so do the prices and with no collateral to provide cover, the stablecoin cannot be redeemed on 1:1 basis relative to its peg. These coins use a combination of above methods e.g. they can be partially crypto collateralized and partially algorithmic OR partially fiat collateralized and partially crypto collateralized and so on. The need for stablecoins in the defi ecosystem stems from the extreme price volatility that cryptocurrencies are subject to. As a result, people and businesses are skeptical of crypto as a valid means of payment as the value of crypto can suddenly decrease in value. Thus, a stablecoin has a better chance of being adopted as global currency and exchange of value. Stablecoins also provide a buffer in the event of a price crash that is common with assets such as bitcoin or Ethereum. Or even if users are holding rapidly declining assets they can swiftly convert to stablecoins to save themselves from losses plus capital gain tax and withdrawal fee. Stablecoins are a good way to motivate new users to adopt crypto as many people consider the volatility of crypto assets as a deterring factor, particularly in regions with economic uncertainty. Stablecoins make a lot of financial activities possible on-chain. These include but are not limited to activities such as lending, crypto trading, derivatives trading, etc. Stablecoins can be used as a day-to-day currency or as payments for commerce activities on a global level saving international payment costs. As these coins reside in contracts, recurring transactions can be programmed making them ideal for salary, premiums, rents, etc. Very few crypto exchanges currently support fiat currencies due to strict regulations. Stablecoins provide a way around this problem by offering crypto-fiat trading pairs by using a fiat-backed stablecoin instead of actual fiat currencies. In this section, we discuss the types of stablecoins and describe their issuing and stability maintenance techniques. As of July 2020, Tether is ranked as the world’s fourth-largest cryptocurrency with a market cap of almost $62 billion Each Tether unit issued is backed in a one-to-one ratio with a unit USD. The fiat currency unit is held in deposit in a bank account by Hong Kong-based Tether Limited. While the original one-to-one asset for Tether was USD, it now includes other collaterals like real-world cash equivalents, assets, and receivables from loans. USDT is available on Bitcoin, Ethereum, and several other blockchains, including TRON, Binance Smart Chain, Polygon, and Ethereum Optimism. USDT relies on arbitrageurs to maintain its peg. When the price of USDT-USD deviates considerably from $1, arbitrageurs bring it back in sync. Arbitrageurs would perform the arbitrage trade whenever the spread would justify the operational costs and perceived risks, and, by doing so, would put upward/downward pressure on USDT pushing it towards $1. When the USDT price in the open market falls below $1, arbitrageurs can buy USDT at that price and sell it back to Tether Treasury for $1. The buying of USDT from the open market and its redemption for USD reduces the supply of Tether in the open market, making the price rise closer to $1. In case USDT rises above $1, arbitrageurs now have the opportunity to buy Tether on a 1:1 dollar basis from the Tether treasury. They can then sell the bought USDT in the open market for the prevailing higher price, making a profit. The resulting increase in the supply of USDT in the market works to bring the price down and closer to $1. The other fiat-backed stablecoins in the top 10 stablecoin list by market cap include USDC, TUSD, and BUSD, which are also 1:1 USD-backed stablecoin. MakerDAO, is a system to leverage digital assets (e.g. $ETH) to generate $DAI, a stablecoin, soft pegged to the US dollar. Once DAI is generated users can spend it freely like any other currency. DAI is issued via a collateralized debt position (CDP), which is similar to taking a collateralized loan. CDPs can be bought with ETH or supported ERC20 tokens and DAI is given in return. Individuals are in essence taking a loan denominated in DAI by depositing their ETH or BAT as collateral. When the loan is paid back, the returned DAI is burned or destroyed. A stability fee similar to interest is charged for taking the loan. The fee can be paid in DAI or MKR, however, it is converted into MKR and burned. By burning the MKR tokens, the system aims to increase the token value by reducing its supply. In essence, this is a “buyback-and-burn” token model in which a network generates income in one currency token and uses the proceeds to buy back and “burn” its own native token to increase its value by reducing supply. Maker has also introduced a variable rate of accrual called the Dai Savings Rate (DSR), earned by staking DAI in the DSR smart contract. The accrual is in the form of DAI that is continuously added to the staker's balance, based on the current DSR. In MakerDAO, the CDP positions are always over-collateralized, so the value of the collateral is always greater in order to cover for any price fluctuations in the collateral. As mentioned above, there are 2 tokens in the makerDAO system; DAI and MKR. The main token is stablecoin DAI and the other token is MKR. The main function of the secondary token is to absorb volatility in the system. DAI aims to always be stable against USD, however, there will always be some form of volatility within the system or in outside markets. This volatility is absorbed by the other token, MKR. In the unlikely event when the market crashes such that the collateralized ETH are no longer able to cover for the debt, MKR is minted and sold in the market to provide cover. In fact, at present, the protocol can sell off MKR tokens to generate off-chain reserves larger than DAI’s entire market cap. These reserves can then be used by makerDAO to stabilize Dai. MKR is also used as a governance token for voting to make decisions regarding various parameters such as stability and fee rate. To maintain the peg, Maker relies on a few mechanisms. One is arbitrage. In the short term, when DAI > $1, arbitrageurs have the incentive to pledge their collateral and issue DAI to make a profit in markets outside of the system. The issuing of DAI increases its supply and brings it back to $1 peg. The opposite is true when DAI falls below $1. In the long term to maintain stability, the system has the option to decrease DAI saving rate (DSR) (earned from depositing DAI in the system) or to decrease stability fee (interest rate) when DAI > $1. When interest or stability fee is low more people are incentivized to borrow leading to issuing of more DAI, thus leading to bringing the price back to $1. When DAI is less than $1, the stability fee is increased, so that the cost of issuing DAI goes up and less DAI is minted, leading to the price going back to $1. In a similar fashion, DSR can be used to manipulate the demand side of DAI and maintain the DAI-USD peg. An increase in the DSR will increase the demand for buying Dai at an exchange, depositing the purchased DAI in the DSR contract, and earning interest. The increase in demand leads to DAI price going up to $1. A decrease in the DSR has the opposite effect, encouraging users to sell DAI to invest elsewhere, resulting in the price going down to $1. Liquity is a decentralized platform that issues stablecoins through borrowing similar to MakerDao, however, it does not charge any interest. The users lock their ETH collateral to create collateralized debt positions (called Troves in Liquity). The system then issues stablecoins called LUSD soft pegged to USD. The minimum collateralization requirement at present is 110%, though a user can set a higher collateral ratio if they prefer. It is advised to keep the collateral ratio at 150%. Liquidity has two tokens, LUSD, which is USD pegged stablecoin and the other is LQTY, which is not meant to be a governance token but is meant to capture value from the system. LQTY's issuance follows an inflationary schedule with the total max supply capped at 100 million. In order to incentivize early adopters, the issuance supply is halved every year. The newly issued LQTY can be earned by either staking LUSD to the protocol or by facilitating LUSD deposits in the staking pool through a front end. Liquity does not have a front end of its own, instead, it is decentralized and anyone can provide a web interface to the end-user enabling them to interact with the Liquity protocol. Both LUSD and LQTY can be staked for rewards (explained below). The protocol does not charge interest but instead charges a one-time fee at the time of issuance and redemption of LUSD. It is important to highlight that there is no governance mechanism in Liquity and there can be no changes made to the system post-deployment. To maintain system solvency, Liquity has a stability pool that acts as an insurance pool. LUSD holders can stake their LUSD in this pool. When a Trove is liquidated for not maintaining the minimum collateral ratio, the stability pool provides liquidity to repay debt from liquidation. LUSD worth the amount of liquidated loan are burned from the pool whereas the collateral held against the said loan in the form of ETH is passed to the stability pool stakers in proportion to their share in the pool. This ensures that the total LUSD supply always remains backed with the required collateral ratio. The incentive or reward for LUSD stakers of the pool is that they receive a greater dollar value of collateral relative to the debt they pay off because Troves are likely to be liquidated at just below 110% collateral ratio. For example, a loan worth 100 LUSD would have a minimum collateral requirement of ETH worth 110 USD. The moment it goes below 110% collateral ratio, this loan is liquidated and 100 LUSD from the pool are burned whereas approx 110 USD worth of ETH collateral held for the liquidated loan is passed on to the stakers in the pool. In essence, for 100 LUSD burned, the stakers gained 110 USD worth of ETH. LUSD stakers also accumulate a reward (in LQTY) proportional to the size of their deposit on a continuous basis. As mentioned above, what makes Liquity different from protocols like Maker are its fee generation and stability mechanisms. Liquity does not charge any interest for the LUSD issued. Instead, it charges one-time borrowing and redemption fees. This fee is distributed to the LQTY stakers based on their proportion in the staking pool. Both fees are algorithmically adjusted and accrue in the form of ETH or LUSD. To boost user confidence in the system, Liquity allows for redeeming LUSD for ETH i.e. any LUSD holder can exchange their coins for ETH at face value (e.g.100 LUSD for $100 worth of ETH). The system achieves this by liquidating the lowest collateralized Troves (even if their collateral ratio is higher than 110%) and transferring the respective amount of ETH to the redeemer. To protect low collateral borrowers who are more vulnerable to redemptions, the system charges a one-off redemption fee that is expected to deter frequent redemptions. This fee is variable and starts at 0%, increases with every redemption, and then decays back to 0% if no redemption is made over time. This dynamic fee also ensures that redemptions are not frequent and do not hurt LUSD stability In order to stabilize the price, Liquity employs the following approaches. As the minimum collateral ratio is 110%, this creates a natural price ceiling for LUSD at $1.10. When the LUSD:USD rate exceeds that level, arbitrageurs can make an instant profit by borrowing the maximum amount against their collateral and selling the LUSD on the market for more than USD 1.10. Even if the loan gets liquidated, the arbitrageur would still make a gain. This activity is expected to steer LUSD away from reaching USD 1.10 and if it ever hits the ceiling, it will rebound very quickly. The system expects that as long as most people believe that 1 LUSD will eventually return to the value of 1 USD, it will have a self-reinforcement effect. When the LUSD price gets above $1, it makes borrowing more attractive (as users can expect to repay at a rate of $1 or lower), whereas when the price moves below $1, it incentivizes repaying existing debts (as this state is likely to be short-lived). When more LUSD is borrowed compared to repayment over time, the total LUSD supply will grow, which should make the tokens cheaper with regard to the USD. Conversely, if the repaid amounts are higher than the new debts, the money supply will shrink, such that LUSD will appreciate. The issuance and redemption fee constitutes an upfront cost that borrowers or redeemers need to pay when they take out a loan or redeem LUSD for ETH. These fees are also used to stabilize prices. Higher issuance fees immediately make new loans less attractive, and thus decrease the generation of LUSD, resulting in LUSD price increasing. Because the issuance fee is an upfront cost, it affects new debts more quickly compared to an interest rate increase, which takes longer to impact supply. Even if a trove is closed due to redemption, that trove’s owner may not be willing to reopen the loan right away as long as the issuance fee remains high. This makes sure that the burned LUSD from redemption is not regenerated immediately, resulting in reduced supply and LUSD rising back to $1. The issuance fee and the redemption mechanism thus work together to stabilize LUSD price. Another stabilizer of prices is the fraction of the entire LUSD supply which resides inside the Stability Pool and is outside regular circulation. However, this pooled fraction of LUSD supply is dependent on the current LUSD:USD exchange rate. When the price of LUSD is higher than USD, the (expected) collateral surplus gains in case of liquidations is lowered, since the system conversion is based on the nominal value of LUSD being equal to USD. As the price of LUSD reaches closer to USD 1.10 (the minimum collateralization ratio), the depositors face an increased risk of a potential loss, and staking in the stability pool becomes less attractive. If the loss risk becomes too high, eventually stakers may withdraw their stability deposits. This will result in more liquidity being injected into the markets by former stability depositors, hence the LUSD price should depreciate. Synthetix is primarily a derivatives platform that issues a stablecoin sUSD to facilitate derivatives trading. The purpose of sUSD is not only to be a stable asset but it is also needed to buy other synthetic assets on the platform. Instead of holding a diversified basket of crypto assets, Synthetix issues its sUSD stablecoin against an over collateralized pile of its own equity token SNX. The value of the sUSD token remains stable primarily through arbitrage. If sUSD is trading below the price of USD, then anyone can profit by buying sUSD cheaply in secondary markets and swapping them within the Synthetix system, as the system always values 1 sUSD for 1 USD. For instance, if the price sUSD token falls to 0.99 USD on secondary markets, a user can buy 100 sUSD with 99 USD, and exchange the sUSD tokens for 100 USD worth of sBTC, or any other synthetic assets on Synthetix platform. This creates a demand for sUSD, leading to the price rising back to 1 USD. Synthetix is currently trialing a new mechanism for additional stability with the dFusion protocol (from Gnosis) in which discounted SNX is sold at auction for ETH, which is then used to purchase sUSD below the peg to jack up its price, details can be found here. Algorithmic stablecoins use algorithms to maintain their peg and control the stablecoin’s market structure. They are synonymous with the Federal Reserve, however, instead of humans making the decisions, it is the pre-programmed code that executes specific actions to stabilize and influence the price. One of the first algo coins is AmpleForth (AMPL). It is pegged to USD and adjusts its supply every 24 hours via a process called rebasing to maintain the peg. In situations where AMPL is above $1, the protocol increases the number of coins in circulation, allowing for the price to return to $1. If demand is low, and the price of AMPL goes below $1, supply is decreased to bring the peg back to $1. This means that if a user held 2% of all AMPL tokens before a rebasing event, they would still hold the same percentage of coins after the rebasing. While AmpleForth has a very simple approach to maintain stability in price, various other stablecoin protocols have taken the concept of algorithmic coins further as shown below. TerraUSD (UST) is an algorithmic stablecoin, which uses LUNA, Terra chain’s native token to issue TerraUSD (UST). Terra chain uses PoS consensus and LUNA is the token validator's stake to be able to verify blocks and earn mining fees. UST is minted by swapping LUNA for UST on the Terra system. When 1 UST is minted, $1 worth of Terra’s LUNA token is taken out of circulation. Terra protocol also issues stablecoins pegged to other regional denominations. Terra ensures UST/USD peg using a circular dual-token system that creates arbitrage opportunities via seigniorage - the value of newly minted UST minus the cost of issuance (which in this case is zero). In seigniorage models, a simpler strategy of stabilizing prices is by controlling the supply of coins in circulation. For example, AmpleForth increases the supply of its coin when it's trading above the peg and conversely, decreases (removed from circulation) when trading below the peg. However, just increasing/decreasing the supply at times can lead to greater price volatility effects on the stablecoin. This is where Terra is different and uses its token LUNA to absorb volatility. LUNA acts as the volatility absorber because it can always be minted at a fixed exchange rate of the system, irrespective of outside market conditions. Arbitrageurs are thus incentivized to ensure that the price returns to its peg. LUNA’s burning mechanism further complements this - a portion of LUNA is burned during expansion to facilitate that the UST is restored to $1. In other words, the price volatility of UST is effectively passed onto LUNA. This is explained further below: Seigniorage — When UST is trading above USD, this means there is a spike in demand for UST and that the supply of UST must increase to compensate for the extra demand. This is known as expansion. To achieve this, the protocol needs to mint and sell UST into the market and relies on the opportunism of individual arbitrageurs who can take profit by purchasing 1 newly minted UST(worth more than its peg) for 1 USD of LUNA, pocketing the difference. This way the value associated with the increased demand in one unit of UST is spread out across newly minted UST, underlaid by the LUNA used to purchase it. In essence, when demand for UST increases, the system mints UST and earns LUNA in return. This value captured through LUNA is now owned by the system, is called seigniorage, and represents the profit gained from minting UST (and it costs next to nothing to mint!). The system burns a portion of earned Luna. A portion of the LUNA is allocated to LUNA validators. The remaining portion of the seigniorage goes to the Treasury whose mandate is to stimulate Terra’s growth and adoption. In this way, the Terra protocol leverages seigniorage to achieve its twin goals of stability and adoption. Contraction — In the opposite case, when the demand for UST falls and results in the price of UST going below USD, the supply of UST needs to be reduced so that the peg is restored. This is known as contraction and is facilitated by the protocol’s own market that always exchanges 1 USD worth of newly minted Luna for 1 UST (which is worth less than 1 UST in secondary markets). In essence, the drop in value from the decrease in the demand of UST is absorbed by LUNA holders because the LUNA supply is increased and the value from LUNA is transferred to UST to bring its price closer to the peg. USDN is built on the Waves blockchain. The Neutrino system consists of 3 tokens namely WAVES, USDN, and NSBT. WAVES is the core utility token of the Waves blockchain that is used for paying transaction fees to miners. It also serves as collateral for USDN, the main Neutrino stablecoin, which is pegged to the US dollar. USDN then serves as collateral for other Neutrino stable assets. NSBT is a recapitalization and governance token of the Neutrino protocol that ensures the USDN collateral reserves’ stability. All Neutrino assets leverage the underlying Waves blockchain’s consensus algorithm to enable staking, which motivates users to own these assets. Users send WAVES to Neutrino’s smart contract, which generates an equal USD value of stablecoins USDN. All WAVES deposited as collateral are then leased to a network node of Waves blockchain to generate revenue via mining rewards. Mining rewards are transferred back to the Neutrino smart contract and automatically converted to USDN tokens. These USDN tokens are then distributed amongst everyone staking USDN or other stable assets. This way users can earn by staking a stablecoin. The stability mechanism of the protocol relies on arbitrage and NSBT Token. When USDN becomes greater than $1, users can exchange WAVES for USDN (1$ per USDN) on the platform. Users then sell this USDN for profit in the open market resulting in increased supply which pushes the USDN price down. Similarly, when USDN is less than $1, users can buy USDN on open exchange for less than 1 USD and exchange them for WAVES in Neutrino exchange at 1 USD value, thus making a profit. In case when the price of collateralized WAVES price grows versus USDN, the smart contract calculates the difference and generates the corresponding amount of USDN. Part of this additional USDN is distributed among the USDN stakers, part is given to the validators, and part is put in a special reserve fund to cover the exchange rate difference should WAVES price decrease in the future. In the Neutrino system, a smart contract dispenses stablecoins in exchange for the underlying crypto and enables the redemption of stablecoins back into crypto. However, it might happen that the redemption of the stablecoin becomes impossible, due to the crypto volatility and the diminishing value of the underlying asset. To counter this, the protocol has added a new instrument called Neutrino system base token (NSBT), which ensures that in case of diminishing reserves in underlying assets there is an incentive to replenish them through the purchase of NSBT. Using a smart contract users can buy NSBT for the ongoing price. The NSBT price depends on the value of the collateral ratio or BR (Backing Ratio). If BR is less than 100%, the discounted price for the purchase of NSBT for WAVES is calculated at a price less than 1 USD with the expectation of future exchange of NSBT for USDN at the value of 1 USD. In other words, users are incentivized to buy NSBT for less than 1 USD and then sell for exactly 1 USD in the future, when BR returns to equal to or greater than 1, and thus make a profit. NSBT is also a stakable asset enabling holders to earn WAVES to USDN swap fees. FEI is an algo coin pegged to USD. There are two tokens in the FEI Protocol. FEI, the stablecoin, has a changing supply model to maintain stability. TRIBE is the governance token that can be used for voting on different kinds of protocol parameters. The FEI stablecoin has an uncapped supply that tracks demand. FEI entered circulation via sale along a bonding curve. This curve approaches and fixes at the $1 peg. When new demand for FEI arises, users can acquire it by buying it from the FEI protocol along the bonding curve. The price function started low to reward early adopters for purchasing FEI. There is no selling bonding curve i.e. users cannot sell FEI for ETH on the bonding curve. Instead, the protocol retains the incoming ETH as Protocol Controlled Value (PCV). Fei Protocol deploys the PCV to create a liquid secondary market (at present in the form of ETH/FEI pool on Uniswap) where users can sell FEI back into ETH. The liquidity pool on Uniswap is special as it is partially owned by the protocol. This is where the PCV or the Protocol Controlled value resides. Fei Protocol achieves the goal of stabilization by incentivizing Uniswap traders with mints (incentives) and burns (taxation). These incentives and taxations are calculated on the basis of FEI’s price distance from the peg. This means that a trader with a large sale will be punished with a large burn. The protocol then incentivizes traders to buy via mint so that the price returns back to the peg. This is done to ensure that all volatility below the peg is net deflationary. The incentives only apply to trades when the spot price is below the peg. The side above the peg is taken care of by the arbitrage loop with the bonding curve of the system as shown below. FEI also has a process to restore the peg in situations where price is below the peg for extended periods by reweighting the Uniswap price back to the peg. It achieves this by executing the following atomic trade: The reweighting process is shown below: These protocols employ a mix of crypto collateralization and algorithmic backing to issue stablecoins Frax or Fractional Algorithmic protocol is a two token system, Frax (FRAX) the stablecoin pegged to USD, and a governance token, Frax Shares (FXS). It employs both collateralization and algorithms to generate stablecoin FRAX. Frax Shares (FXS) is the token that accrues fees, seigniorage revenue, and excess collateral value. In order to hold the collateral, the protocol has a pool that maintains USDC reserves. The system has the flexibility to add other collateral pools with governance voting. Users can mint FRAX by providing two tokens: a collateral token, currently USDC, and the protocol’s share token FXS. The proportions are given by the collateral ratio. For example, a 60% ratio means that $1 FRAX can be minted with $0.60 USDC and $0.40 FXS. FRAX can always be redeemed for $1. To continue the example with a 60% collateral ratio, each FRAX is redeemable for $0.60 of collateral and $0.40 of FXS. Both minting and redeeming operations have fees that generate revenue for the protocol. It is the above two-way convertibility of FRAX (issuing and redeeming) that guarantees its peg with USD, e.g. To elaborate on the above points, if the market price of FRAX falls below $1, then there is an arbitrage opportunity to redeem FRAX tokens by purchasing them cheaply on the open market and redeeming FRAX for $1 of value (USDC+FXS) from the system. A user is always able to redeem FRAX for $1 worth of value from the system. The difference is simply what proportion of the collateral and FXS is returned to the user. To account for strong market contraction, the system is protected by several buffers. First, the protocol increases the collateralization ratio during phases when demand for FRAX is low, meaning that FRAX is trading below $1. Through re-collateralization, the redeemers of FRAX get more USDC and less FXS. This in turn is expected to boost market confidence and increase the demand of FRAX as its underlying asset proportion of USDC increases. Second, many liquidity providers have been incentivized to voluntarily lock their liquidity in pools for several years in exchange for a higher return. For example, more than half of LP tokens in the FRAX/FXS pool are locked for several years. By being out of circulation, they ensure price stability. Third, the protocol also has a feature to issue FRAX bonds (FXB) - discounted securities priced less than $1. In the event of rapid selling of FRAX, FXB is issued to incentivize FRAX holders to buy the bonds instead of continuing to sell FRAX against USDC and FXS. The issuance of bonds is stopped as soon as the sell pressure alleviates. Bondholders benefit from buying FXB below $1 and by redeeming them for $1 at maturity. While stablecoins present many advantages, they also have their limitations and risks. Fiat-backed stablecoins such as Tether are centralized, meaning they are run by a single entity. This means users need to trust that this entity has 1:1 backup for stablecoins with real fiat. Users therefore must look at regular audits from third parties to ensure transparency and maintain trust. Centralized stablecoins are also constrained by regulations that come with fiat currency such as capital gain tax, compromising the efficiency of the conversion process and the potential efficacy of the digital asset. Since fiat-backed coins are more regulated, they also have less liquidity than regular cryptocurrencies. This is especially true for commodity-backed stablecoins. For example, if a user wanted to get back their gold collateral it could take months. Crypto-backed stablecoins have their own set of issues. As they are pegged to other cryptocurrencies, this makes them much more vulnerable to price volatility in comparison to fiat or commodity-backed stablecoins. In the event of a price crash or black swan event, they are expected to be auto-liquidated into the underlying crypto asset, where they won’t be stable at all. Another problem of crypto-collateralized stablecoins is that they’re difficult to understand by a regular user. Stablecoins such as DAI also has scalability issues and capital inefficiency issues along with dependence on user's demand for debt. Most algorithmic coins rely on manipulating supply to maintain price stability. The algorithm calculates how much excess supply is optimal, and burns or issues up the amount needed to bring the price back up to $1 exactly. Though this appears efficient, there are issues here as well. For starters, this doesn’t work during a crash when there is a sudden major drop in demand. In a scenario where the market crashes and users pull out a significant amount of money from the stablecoin, the algorithm would be instructed to buy up enough supply to bring the price back up to $1. But what happens if there isn’t any future demand for the coin due to the crash and loss of user confidence. So the model crashes if there is no sustainable future demand. Further, the systems of these algorithmic protocols are often incredibly complex and difficult to execute, making them unreliable to gain the trust of the user majority. This is reflected in the fact that currently, stablecoins have much lesser market caps compared to fiat or crypto-backed coins. Regulations are a big problem for not just stablecoins but for crypto assets in general. Towards the end of 2019, when stablecoins were just emerging, the G7 summit strongly raised its concerns about the risks involved in using them in international settlement transactions. Most of these risks stem from issues such as money laundering, taxation, and terrorism financing. There is also the unpredictability issue with regulations. Regulators can suddenly decide against crypto and crash an exchange (as they did with OKEx) and shut them down either temporarily or permanently. And since users don’t have any legal binding to the fiat collateral stored at these exchanges there isn’t much they can do. This was recently experienced by the UK users of Binance who could not pull their fiat out of the exchange after it was banned in the UK. Stablecoins create possibilities of a world in which digital payments are frictionless and instantaneous without the loss in value. While still a relatively new asset class, stablecoins have proven to be a major component of the defi ecosystem. Having trading volume in the hundreds of billions, and market cap in the billions, stablecoins could become the core building blocks on which future financial products and systems are built. However, it is yet to be seen how regulators respond to stablecoins, and how much they welcome them. This may therefore impact the success and adoption of stablecoins. Stably. “The Real Risks of Moving All Your Assets INTO STABLECOINS.” Medium, Stably, 12 Mar. 2021, medium.com/stably-blog/the-real-risks-of-moving-all-your-assets-into-stablecoins-dee42cda25de. Tether Arbitrage & The Dollar Peg. Medium. (2021). Retrieved 22 August 2021, from https://medium.com/@alexkruger/tether-arbitrage-the-dollar-peg-7da405f13ffc. Stablecoins — Defining the Terra Algorithmic Design. Medium. (2021). Retrieved 22 August 2021, from https://medium.com/terra-money/stablecoins-defining-the-terra-algorithmic-design-5d952fdf68d. (2021). Retrieved 22 August 2021, from https://www.coinspeaker.com/guides/what-is-terrausd-ust-stablecoin/. Neutrino Protocol Overview. Medium. (2021). Retrieved 22 August 2021, from https://stackingventures.medium.com/neutrino-protocol-overview-ceba84cc88e4. FRAX, a partially collateralized stablecoin. Medium. (2021). Retrieved 22 August 2021, from https://medium.com/coinmonks/frax-a-partially-collateralized-stablecoin-53d7841a4558. Overview. Docs.fei.money. (2021). Retrieved 22 August 2021, from https://docs.fei.money/. Social Network for Programmers and Developers. Morioh.com. (2021). Retrieved 22 August 2021, from https://morioh.com/p/42f4fc457235 Terra Docs | Terra Docs. Docs.terra.money. (2021). Retrieved 22 August 2021, from https://docs.terra.money/. MakerDAO Documentation. Docs.makerdao.com. (2021). Retrieved 22 August 2021, from https://docs.makerdao.com/. Frax: Fractional-Algorithmic Stablecoin Protocol. Docs.frax.finance. (2021). Retrieved 22 August 2021, from https://docs.frax.finance/. Team, S. (2021). Synthetix System Documentation. Docs.synthetix.io. Retrieved 22 August 2021, from https://docs.synthetix.io/litepaper/.Stablecoins

Types Of Stablecoins

Collateralized

Fiat-Collateralized Stablecoins

Commodity-Collateralized Stablecoins

Crypto-Collateralized Stablecoins

Algorithmic, Non-Collateralized

Hybrid

Value Created By Stablecoins

Top Stablecoins By Market Cap - Issuance And Stability Processes

Fiat-backed

USDT (TETHER)

Crypto-backed

DAI

LUSD (No-Interest Stablecoin)

sUSD

Algorithm-backed

UST

USDN

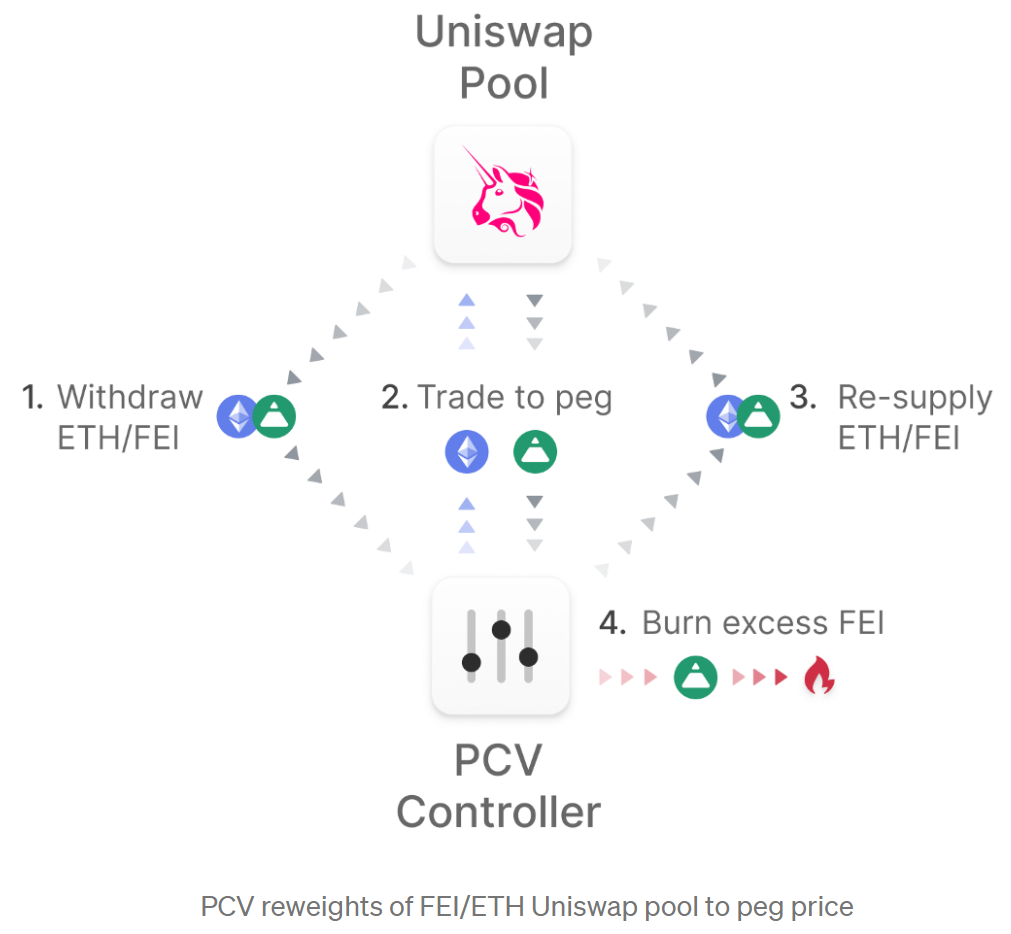

FEI

Hybrid

FRAX

Limitations Of Stablecoins

Regulatory Concerns Around Stablecoins

Conclusion

References

Top stablecoin tokens by market capitalization. CoinMarketCap. (n.d.). https://coinmarketcap.com/view/stablecoin/.

JY, L., 2021. EP 53: Basic Primer to Token Design of DAI (MakerDAO) | The OG Stablecoin. [online] Linkedin.com. Available at: <https://www.linkedin.com/pulse/ep-53-basic-primer-token-design-dai-makerdao-og-stablecoin-tan> [Accessed 22 August 2021].

Liquity. (2021). Official Liquity Documentation. Docs.liquity.org. Retrieved 22 August 2021, from https://docs.liquity.org/.

Liquity: Decentralized Borrowing. Medium. (2021). Retrieved 22 August 2021, from https://medium.com/liquity/liquity-decentralized-borrowing-5a4b0eb28efc.

NSBT asset. Support.waves.exchange. (2021). Retrieved 22 August 2021, from https://support.waves.exchange/en/articles/4535034-nsbt-asset.

Also read, Synthetix: Derivatives On The Blocks

We develop cutting-edge products for the Web3 ecosystem supported by our extensive research on blockchain core and infrastructure.